Understanding the Basics: How Term Life Insurance Protects Your Family

Term life insurance is a vital financial tool that provides your family with peace of mind in case of unforeseen circumstances. It functions by offering coverage for a specified period, usually ranging from 10 to 30 years. During this time, if the insured individual passes away, a predetermined death benefit is paid to the designated beneficiaries. This benefit can help cover essential expenses such as mortgage payments, education costs, and daily living expenses, ensuring that your family’s financial stability is protected in your absence.

Understanding how term life insurance works is essential for making informed decisions about your family's future. Here are a few key aspects to consider:

- Affordability: Term life insurance is typically more cost-effective than permanent life insurance policies, allowing you to obtain higher coverage amounts for lower premiums.

- Flexibility: Many term life policies offer the option to convert to permanent insurance or renew at the end of the term, providing options as your family's needs evolve.

Is Term Life Insurance the Right Choice for Your Family's Safety Net?

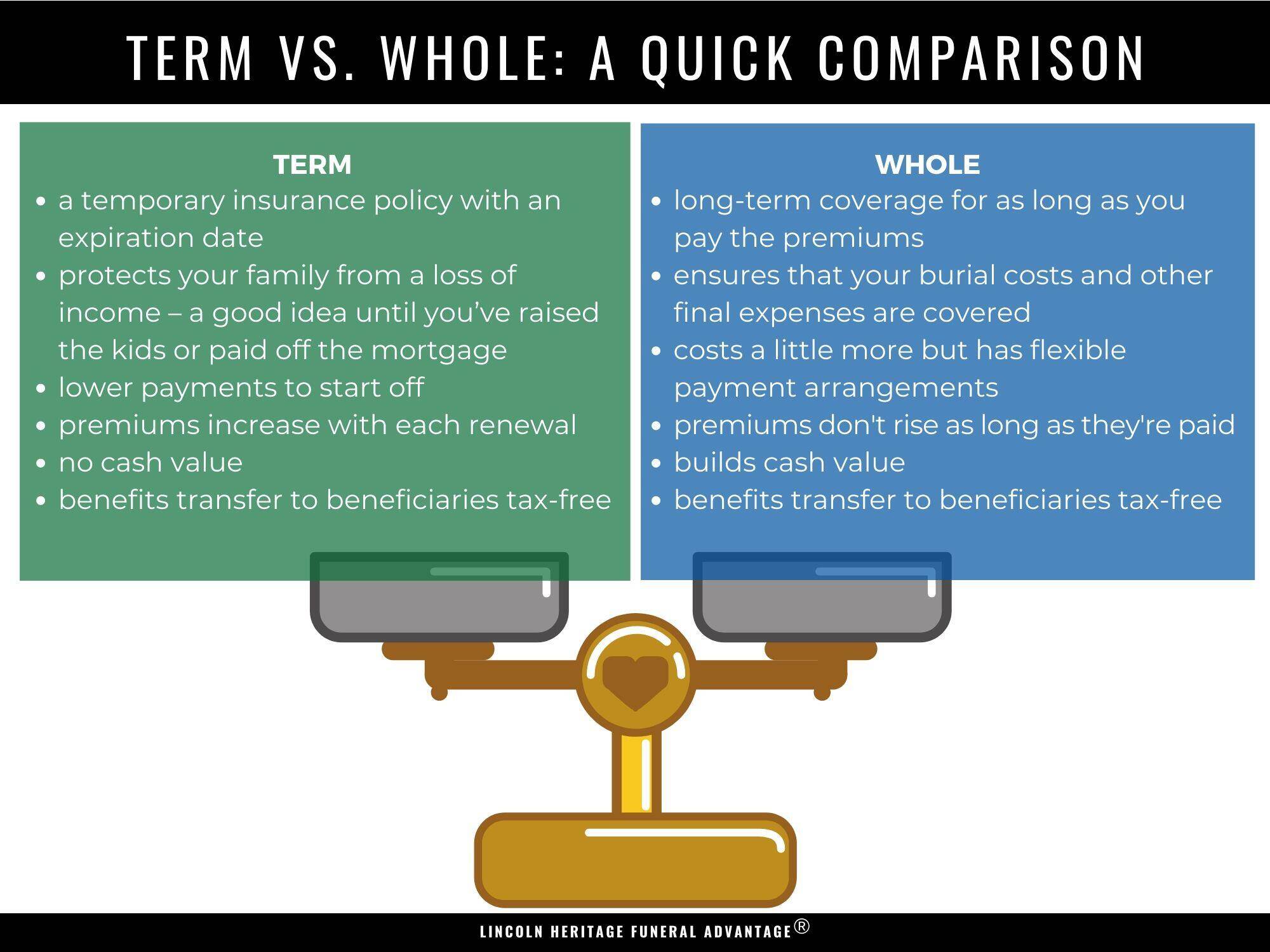

Term life insurance can serve as a valuable safety net for families, providing financial protection during pivotal years when dependents rely heavily on a primary earner's income. Unlike whole life insurance, which offers lifelong coverage, term life policies provide coverage for a specific duration, typically ranging from 10 to 30 years. This makes them a more affordable option for families seeking peace of mind without breaking the bank. By securing a policy that aligns with your family's needs, you can ensure that in the event of an unexpected loss, your loved ones will have the financial resources to cover living expenses, debt repayments, and educational costs.

When considering whether term life insurance is the right choice for your family's safety net, it's essential to evaluate your specific financial situation and future goals. Here are a few factors to consider:

- Dependents' Needs: Assess how much coverage your family would require to maintain their current lifestyle in your absence.

- Debt Obligations: Factor in any outstanding debts, such as a mortgage or student loans, that your loved ones would need to settle.

- Future Expenses: Consider additional financial responsibilities like college tuition for children.

Comparing Financial Safety Nets: Why Term Life Insurance Stands Out

When evaluating financial safety nets, term life insurance consistently emerges as a frontrunner among various options. Unlike permanent life insurance, which accumulates cash value over time, term life provides pure life coverage for a specified period, often at a lower cost. This affordability allows policyholders to secure substantial death benefits during critical years, such as when raising children or paying off a mortgage. Moreover, since the coverage is temporary, families can reassess their needs and adjust their financial strategies as their circumstances evolve.

What truly sets term life insurance apart from other financial safety nets is its simplicity and clarity. With straightforward policies and defined terms, individuals can easily understand the benefits and obligations involved. Additionally, premiums are often fixed, allowing for predictable budgeting without unexpected costs. In times of financial uncertainty, having a solid plan like term life insurance brings peace of mind, ensuring that loved ones remain financially secure should the unexpected occur, thus showcasing it as a reliable choice for modern financial planning.